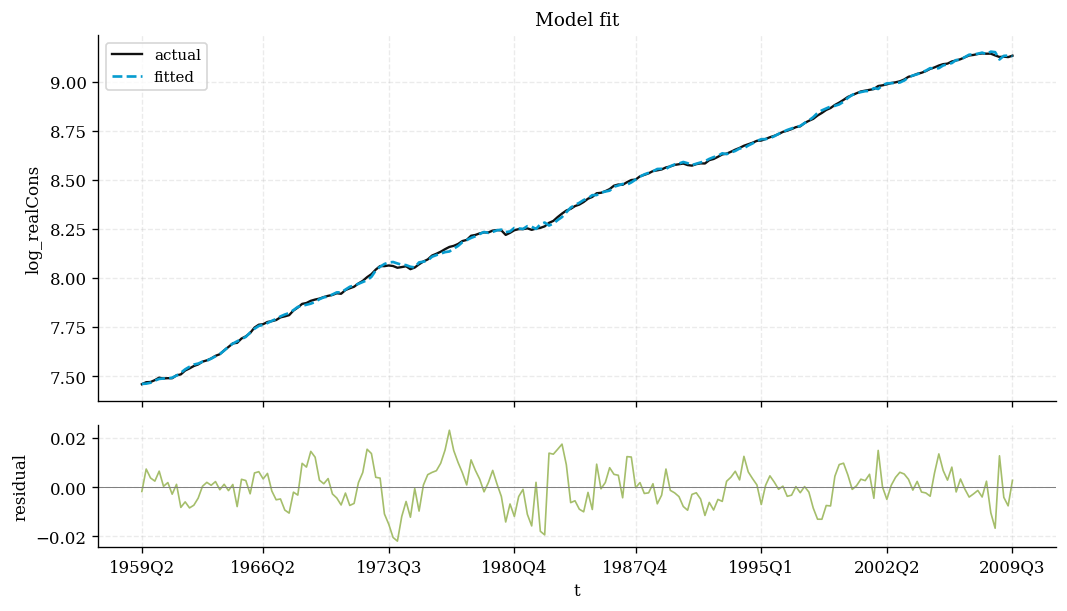

A little theory

Based on Hall, S. G., Swamy, P. A. V. B. & Tavlas, G. S. (2015),

A Note on Generalizing the Concept of Cointegration.

Any (possibly nonlinear) structural relationship \(y_t=f_t(x_t,w_t)\) can be

represented exactly as a model that is linear in variables but with

time-varying coefficients:

$$ y_t=\gamma_{0t}+\gamma_{1t}x_{1t}+\dots+\gamma_{K-1,t}x_{K-1,t} $$

Each coefficient is driven by observable coefficient drivers

\(z_{dt}\) plus a random error (Assumption 1):

$$ \gamma_{jt}=\pi_{j0}+\sum_{d}\pi_{jd}\,z_{dt}+\varepsilon_{jt} $$

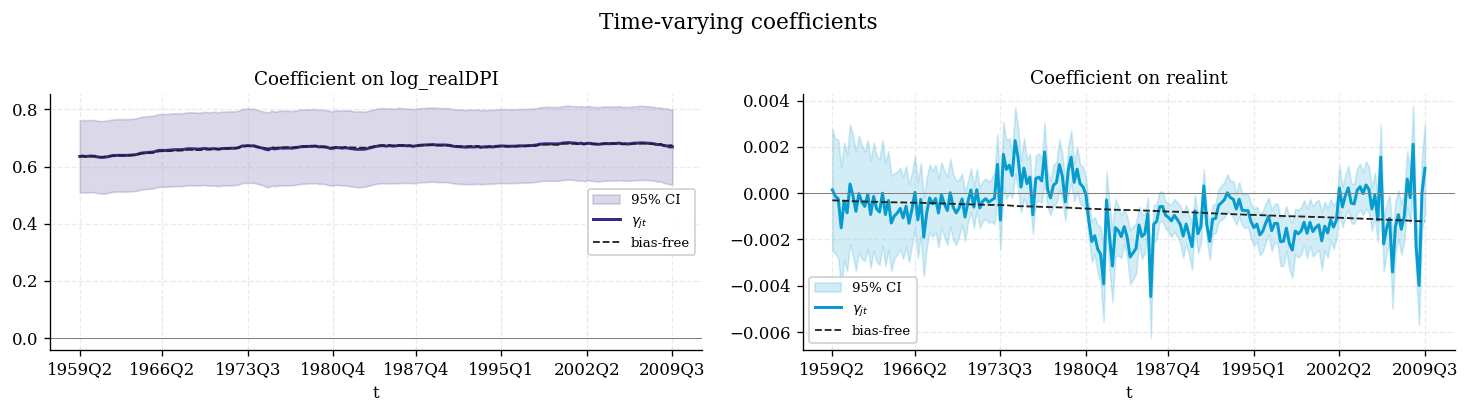

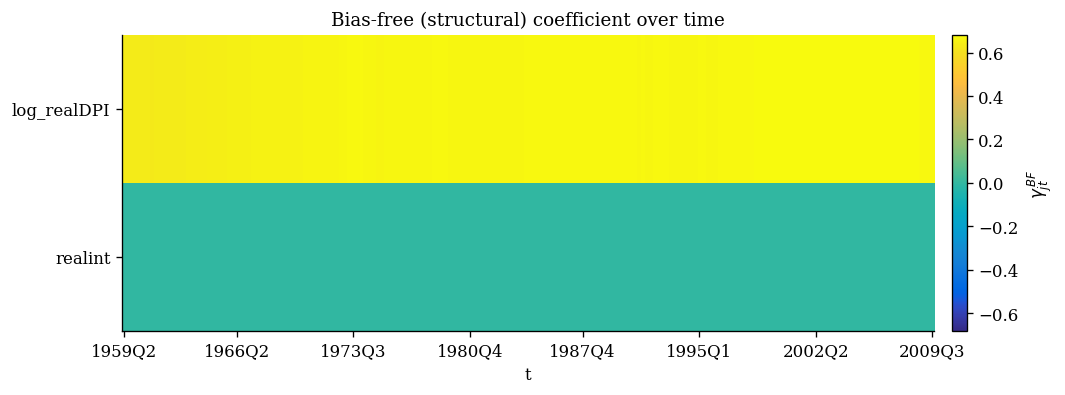

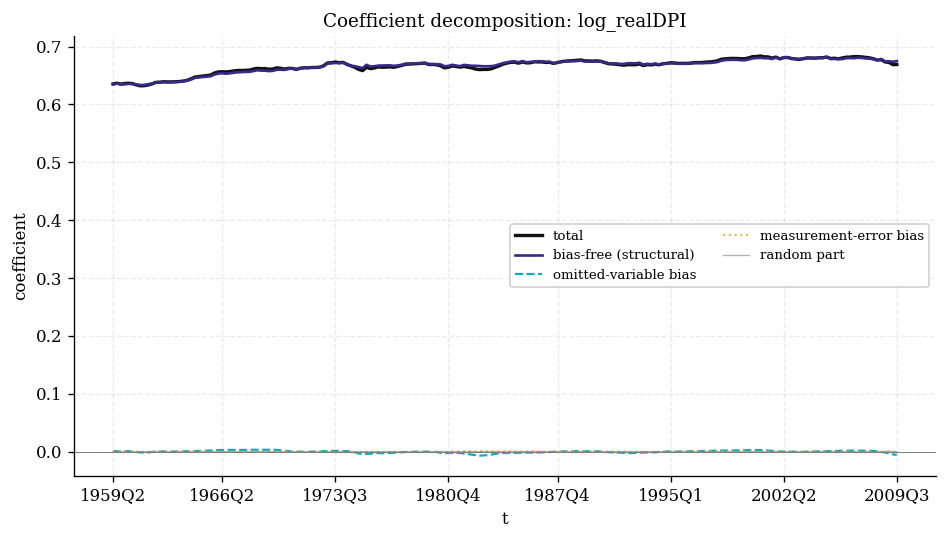

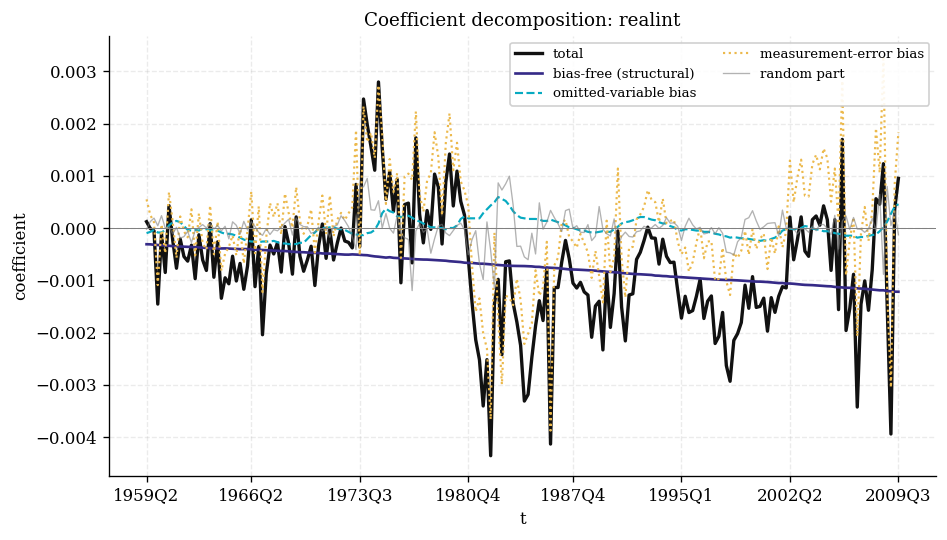

The drivers are split into three sets so the coefficient decomposes into a

bias-free structural part plus omitted-variable

and measurement-error biases. Two variables are

generalized-cointegrated when — holding all other relevant

preexisting conditions \(w\) constant — the bias-free part of the derivative is

nonzero:

$$ \frac{\partial y_t}{\partial x_t}\neq 0 \quad\Longleftrightarrow\quad \text{generalized cointegration.} $$

Substituting the driver equations into the model yields a concentrated linear

model \(y_t=w_t'\pi+u_t\) with a heteroskedastic but stationary

error, estimated by iteratively rescaled GLS. Because the test

statistic derives from the stationary driver-equation errors, inference is

standard — no unit-root critical values.

Honest caveat. As in the paper, validity rests

on choosing drivers that genuinely span the bias components (Assumption 1).

This is an identifying assumption, not something the data can confirm — pick

drivers plausibly correlated with the suspected misspecification.