🔬 PyCupFM¶

Panel Cointegration with Common Factors

Python implementation of all 5 estimators from Bai, Kao & Ng (2009, Journal of Econometrics)

and Bai & Kao (2005)

📦 Install in one line¶

pip install pycupfm

✨ Features at a Glance¶

5 Estimators¶

LSDV, Bai FM, CupFM ★, CupFM-bar, CupBC — faithfully translated from the original GAUSS source code

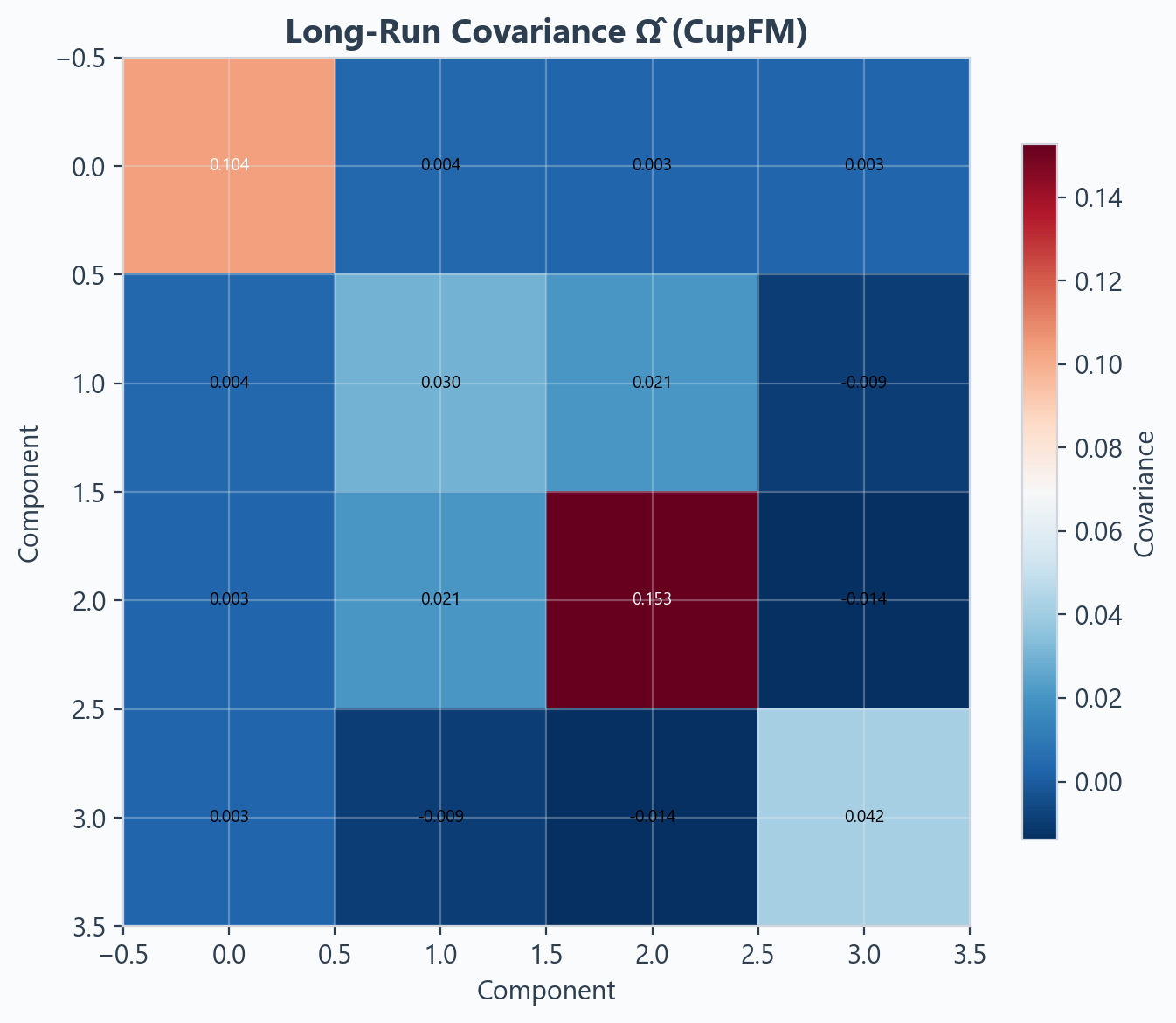

Beautiful Visualizations¶

9 publication-quality plot types with premium academic aesthetics using matplotlib

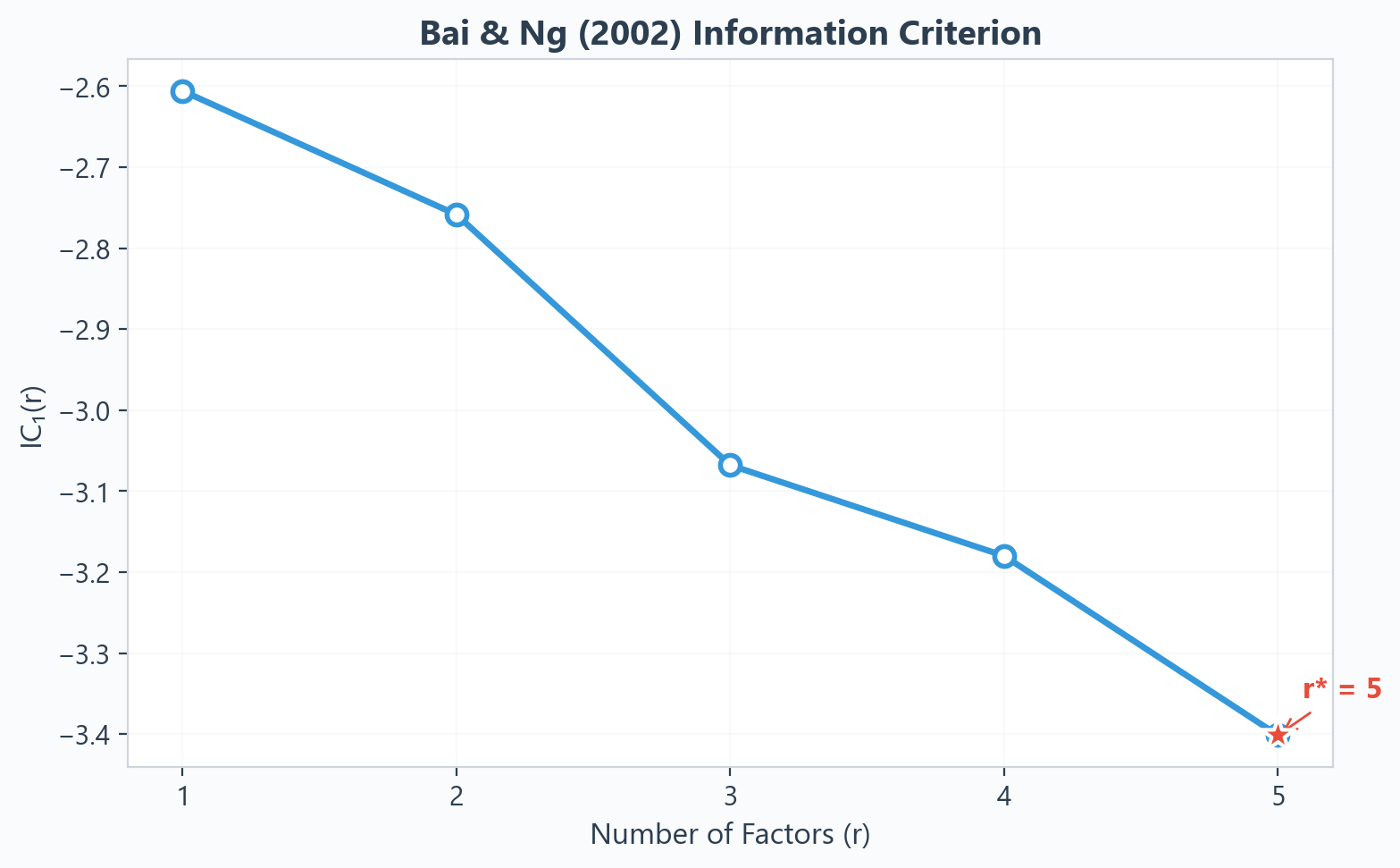

Auto Factor Selection¶

Bai & Ng (2002) IC for automatic factor number selection + auto-bandwidth

Export Everywhere¶

LaTeX, Excel, CSV, HTML tables — ready for your next paper submission

Monte Carlo Tools¶

Built-in DGP simulation replicating BKN (2009) Tables 1-4

Pandas Native¶

DataFrame input/output with automatic variable name inference

🚀 Quick Start — 5 Lines of Code¶

from pycupfm import CupFM

from pycupfm.datasets import load_grunfeld

df = load_grunfeld() # N=10 firms, T=20 years

model = CupFM(n_factors=1, bandwidth=3, max_iter=25)

results = model.fit(

y=df['linvest'], X=df[['lmvalue', 'lkstock']],

panel_id=df['firm'], time_id=df['year'],

var_names=['lmvalue', 'lkstock'], dep_var='linvest'

)

results.summary()

📊 Output — Publication-Quality Summary Table¶

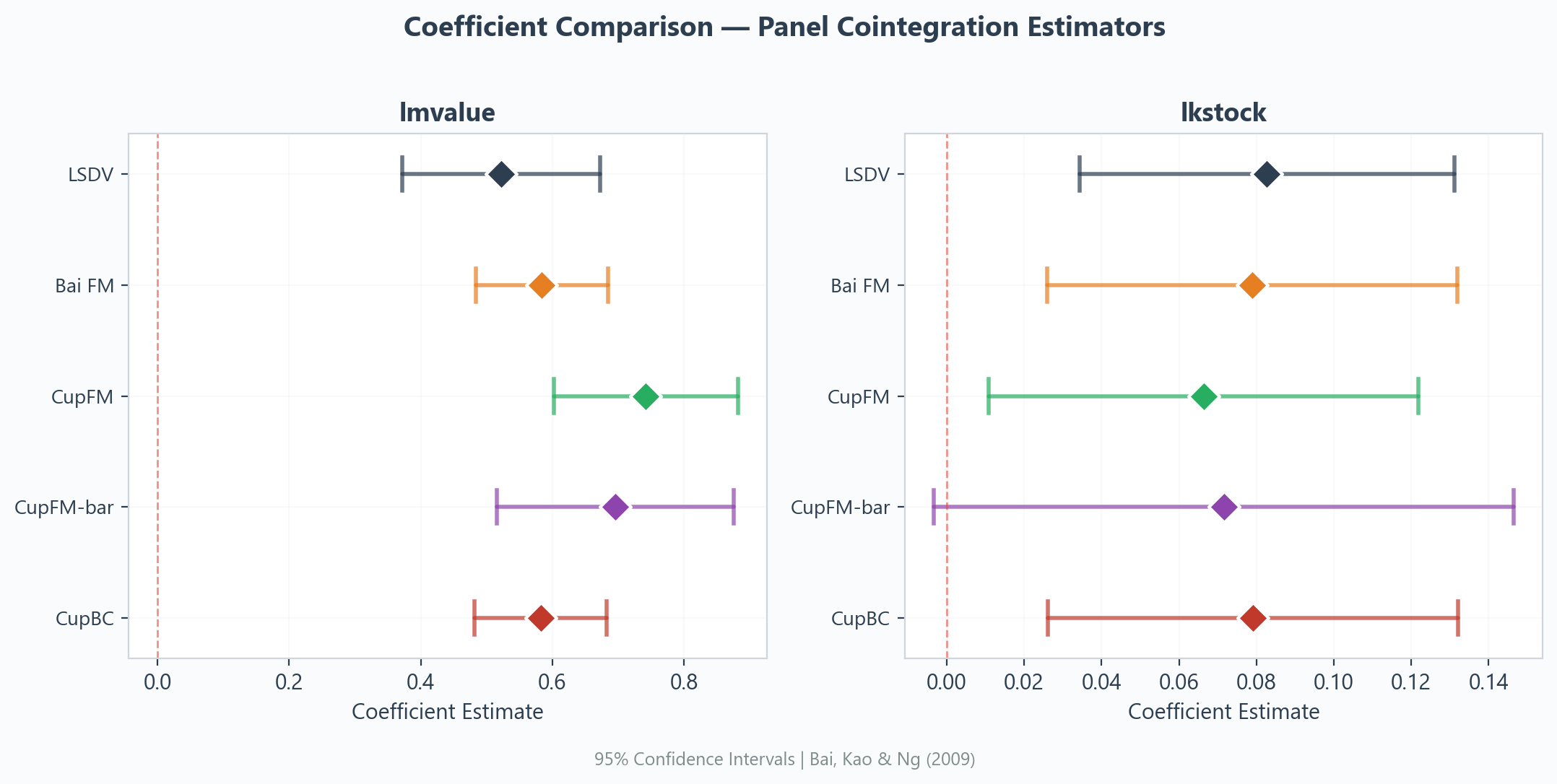

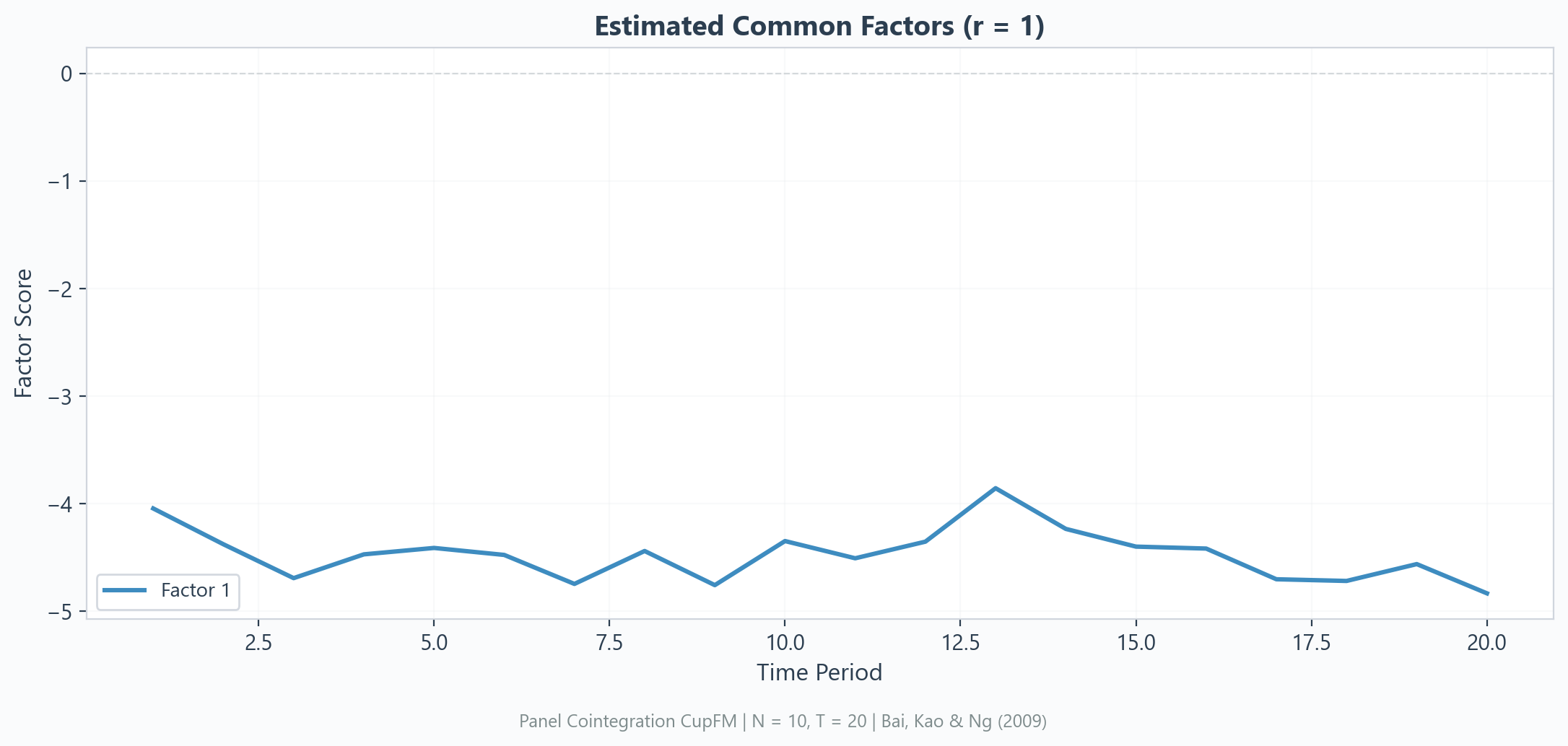

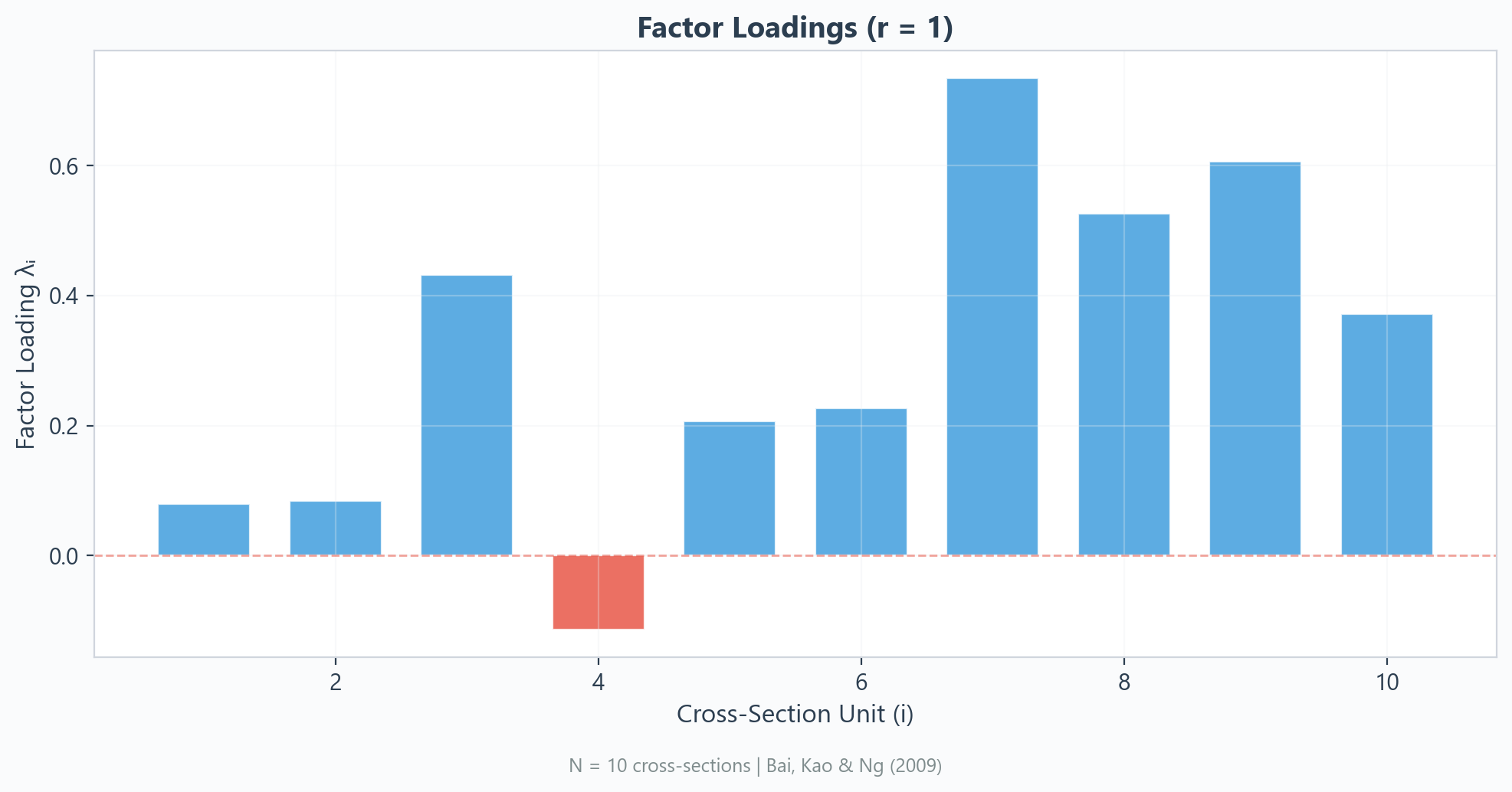

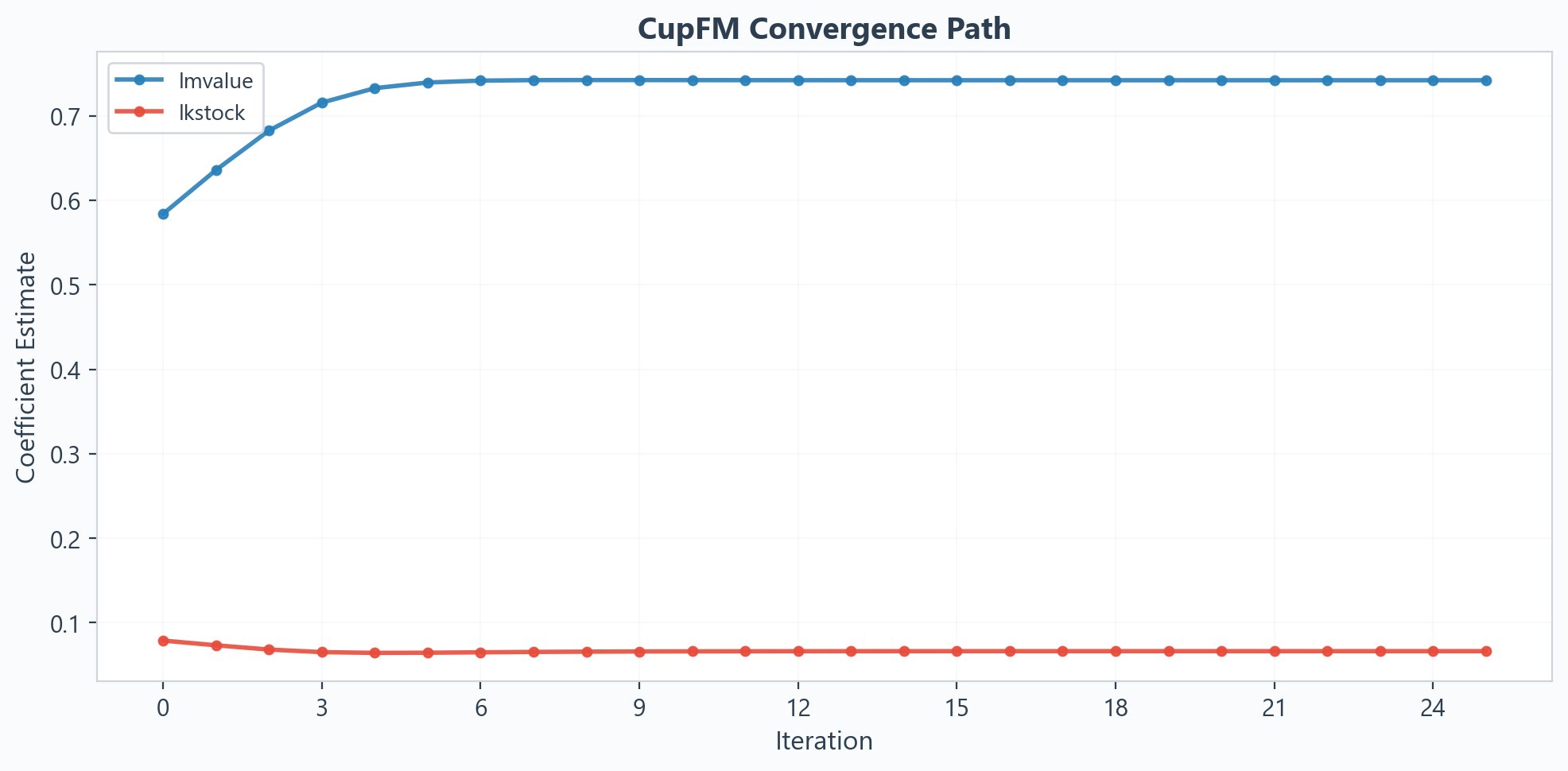

🎨 Visualization Gallery¶

📐 The Model¶

Panel cointegrating regression with common factor structure:

where \(F_t\) are \(r\) common I(1) stochastic trends and \(\lambda_i\) are heterogeneous loadings.

| Estimator | Method | Iterates | Reference | Status |

|---|---|---|---|---|

| LSDV | Within / FE | ✗ | Biased baseline | ⚠️ Biased |

| Bai FM | FM correction (1-step) | ✗ | Bai & Kao (2005) | ✅ Consistent |

| CupFM ★ | FM + continuous updating | ✓ | BKN (2009) Thm 3 | ⭐ Recommended |

| CupFM-bar | FM + Z-bar instrument | ✓ | BKN (2009) | ✅ Consistent |

| CupBC | BC + updating | ✓ | BKN (2009) Thm 2 | ✅ Consistent |